AI agents are rewriting insurance from the inside out

CB Insights' 2025 Insurtech 50 list reads less like a roster of incremental improvers and more like a battlefield map of an industry in transformation.

CB Insights' 2025 Insurtech 50 list reads less like a roster of incremental improvers and more like a battlefield map of an industry in transformation.

Underwriters used to spend days, sometimes weeks, parsing hundred-page documents to make a single coverage decision. Now they're doing it in minutes. AI agents are extracting data, assessing risk, and generating tailored policies faster than humans thought possible. This isn't future speculation. It's happening now, and it's why CB Insights' 2025 Insurtech 50 list reads less like a roster of incremental improvers and more like a battlefield map of an industry in transformation.

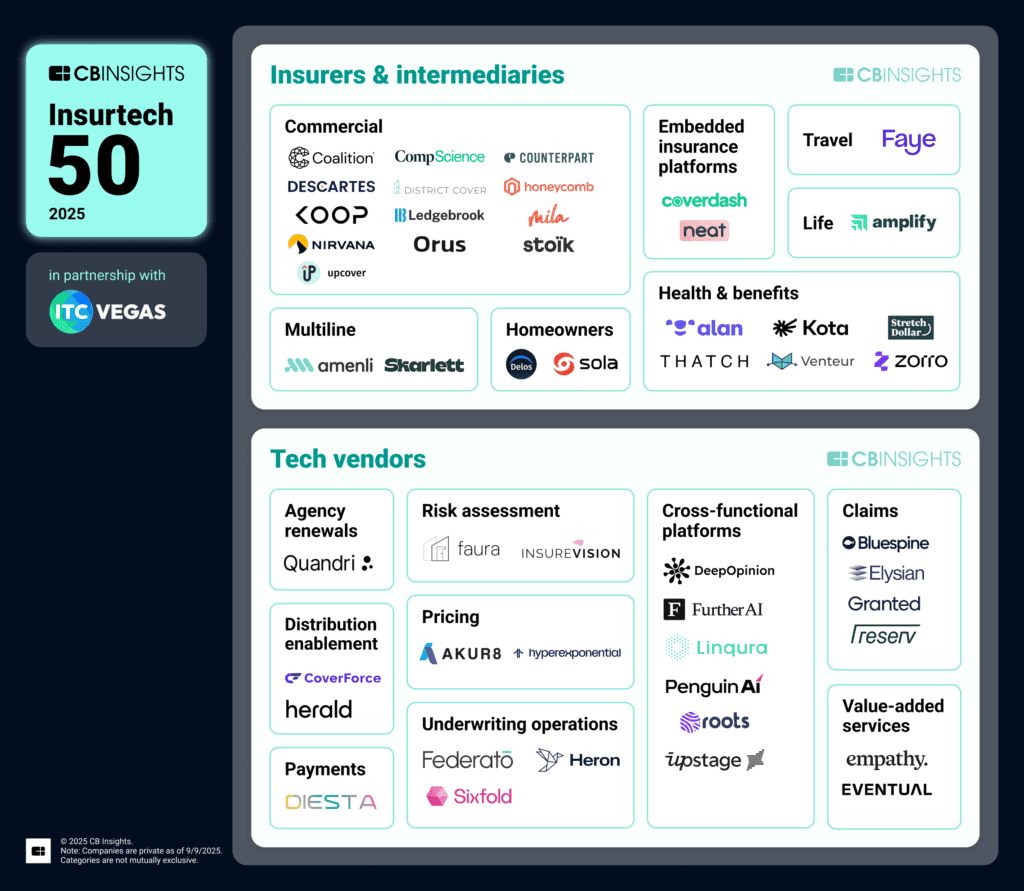

Released October 18 at InsureTech Connect in Las Vegas, the list spotlights 50 startups that represent the top 3% of private companies globally. These companies have collectively raised $3.6 billion. Sixty per cent are early-stage, a 20-percentage point increase from last year. Nearly three-quarters weren't in business at the start of this decade. The message is clear: investors and industry leaders believe the real disruption is just starting, and they're betting on companies young enough to be built from scratch around AI.

The report identifies two macro forces driving innovation: AI agent commercialisation and extreme weather events. While climate change grabs headlines with $101.4 billion in US disaster losses in the first half of 2025 alone, it's AI that's fundamentally rewriting how insurance operates day to day.

The automation wave is hitting underwriting

Insurance has always been a knowledge-intensive business. Underwriters evaluate risk by synthesising information from dozens of sources: financial statements, property inspections, historical claims data, and regulatory filings. The bottleneck wasn't finding information; it was processing it fast enough to make competitive offers.

AI is obliterating that bottleneck. Companies like Allianz are deploying generative AI tools that scan documents, extract relevant data points, and surface insights in seconds. What used to take an underwriter three days can now happen before lunch. The competitive advantage is obvious: faster quotes mean more business, especially in commercial lines where speed determines who wins the client.

But speed is just the first-order effect. The more profound transformation is in capacity expansion. When underwriting gets 10x faster, insurers can evaluate risks they previously ignored. Not because those risks were too dangerous, but because they were too time-consuming to assess profitably. AI doesn't just accelerate existing workflows; it makes entirely new markets economically viable.

The 2025 Insurtech 50 reflects this shift. The list includes 23 tech vendors alongside 27 insurers and intermediaries. Those vendors are building the infrastructure that makes AI-powered underwriting possible: platforms for document intelligence, risk modelling engines trained on decades of claims data, and agent frameworks that handle routine decisions autonomously while flagging edge cases for human review.

The playbook beyond underwriting

While underwriting gets the most attention, AI is transforming every part of the insurance value chain. Claims processing, historically a labour-intensive nightmare of paperwork and phone calls, is being automated end-to-end. Customers file claims through mobile apps, AI agents assess damage from photos and sensor data, and payouts happen in days instead of weeks.

Customer service is being augmented with AI agents that handle routine inquiries like policy changes, coverage questions, and billing issues without human intervention. This isn't replacing humans entirely; it's freeing them to handle complex situations that require judgment and empathy.

The pattern across the Insurtech 50 winners is consistent: find a manual, high-touch process that's ripe for automation, build AI agents that handle 80% of cases, and use humans for the remaining 20% that require nuance. This hybrid model is proving more effective than either pure automation or pure human service.

Startups exploiting the AI advantage

Thatch, ranked fifth, is leveraging technology to make Individual Coverage Health Reimbursement Arrangements (ICHRA) actually navigable. Employer-sponsored health insurance is notoriously complex, but ICHRA adds another layer by shifting choice to employees. Thatch uses AI to guide employees through plan selection, ensuring they get appropriate coverage without drowning in options. CEO Chris Ellis says the goal is "building a healthcare system people love." Automation is what makes personalised guidance economically feasible at scale.

Ledgebrook is bringing technology to the excess and surplus (E&S) market, a historically relationship-driven, manual segment of insurance. E&S covers risks that standard insurers won't touch: unusual properties, high-risk businesses, complex liability scenarios. By combining AI-powered risk assessment with exceptional broker service, Ledgebrook is proving that even relationship-intensive markets can be automated without losing the human touch that closes deals.

Venteur is another ICHRA platform using automation to make employer health benefits accessible to businesses of all sizes. The company focuses on intuitive software, compliance expertise, and personalised support, all delivered through technology that makes a traditionally high-touch service model scalable.

The ICHRA angle is particularly revealing. Multiple Insurtech 50 winners are attacking this space because regulatory change (ICHRA rules that took effect in 2020), combined with AI automation, has opened a window that didn't exist five years ago. This is the pattern to watch: find areas where regulation creates new possibilities, then use AI to deliver services that would be economically impossible with pure human labour.

The competitive pressure is building

The insurance industry is facing a paradox. On one hand, catastrophic losses are mounting. $101.4 billion in the first half of 2025 alone. On the other hand, commercial insurance rates fell 4% globally in Q2 2025, the largest quarterly drop in recent years and a reversal of a seven-year upward trend.

How do you reconcile rising risk with falling prices? The answer is capacity expansion through automation. When AI compresses underwriting timelines and expands the range of risks insurers can profitably assess, supply increases. More supply means greater pricing pressure. Companies that can't match the operational efficiency of AI-powered competitors will get squeezed on margins until they either adapt or exit.

This explains why 60% of the Insurtech 50 are early-stage companies. Investors are betting that startups built from scratch on modern AI infrastructure will outcompete incumbents burdened by legacy systems and manual processes. Nearly three-quarters of the winners weren't in business at the start of the decade. They're greenfield operations unencumbered by 50 years of accumulated technical debt.

CB Insights analyst Chris Sekerak put it bluntly: "These new entrants are shaping a competitive landscape where AI agents augment operations and customers gain more coverage choices." Not "might shape" or "could shape." Are shaping. Present tense. It's happening now.

The infrastructure being built

The broader story isn't just about individual companies. It's about the infrastructure layer being built to support an AI-native insurance industry.

Document intelligence platforms are learning to extract structured data from unstructured sources like inspection reports, medical records, and legal filings. Risk modelling engines are being trained on decades of claims data to predict losses with greater accuracy than human underwriters. Agent frameworks are handling routine decisions autonomously while maintaining audit trails for compliance.

This infrastructure will compound. Every AI-processed claim decision creates training data that makes the next decision more accurate. Every underwriting model deployed improves with each policy written. The companies building this infrastructure (many of them on the Insurtech 50 list) are establishing feedback loops that get stronger over time.

What insurers must do now

For incumbents, the path forward is stark: aggressively adopt AI automation or watch startups capture market share by offering faster quotes, better prices, and superior customer experiences.

The good news is that insurance has one advantage many industries lack: massive amounts of structured historical data. Every claim paid, every policy written, every loss assessed is training data for AI models. Companies sitting on decades of this data have an asset that can't be easily replicated.

The bad news is that data alone doesn't matter without the technical capability to use it. Legacy systems built in the 1990s weren't designed for machine learning workloads. Integrating AI into existing workflows requires both technical investment and cultural change, neither of which happens quickly at large organisations.

The Insurtech 50 represents the companies betting they can move faster than incumbents can adapt. With $3.6 billion in funding and a 60% concentration in early-stage companies, the smart money thinks they're right.

Insurance is being rewritten in code. The question is who writes it.